Electric and plug-in hybrid car sales rankings

Showing posts with label SAIC. Show all posts

Showing posts with label SAIC. Show all posts

Friday, July 11, 2025

Tuesday, February 11, 2025

World EV Sales - Full Year 2024 (OEMs)

My bets for the 2025 top 5 OEMs:

xEV

- BYD

- Geely

- Tesla

- SAIC

- VW Group

BEV

- BYD

- Tesla

- Geely

- SAIC

- VW Group

What are your bets?

Monday, May 3, 2021

2021 Q1 Sales by OEM

Looking at the Q1 2021 sales by Automotive Group, we have:

PHEV+BEV

If we gather plugin sales by Automotive Groups, Tesla ended the first quarter of the year in the lead, with 16% share, 3% less than a year ago, which nevertheless is still a small feat all by itself, considering the intensive diversification process that the EV world is now having, 16% is still significant.

Tesla's current domination is however being threatened by the Volkswagen Group the rise and rise of SAIC, that jumped from #9 in Q1 2020, to the current 2nd spot, with its share jumping from 4% a year ago, to the current 13%.

Although most of this growth has to do with the Wuling Mini EV success story, the truth is that SAIC itself is also benefiting from the export efforts made through MG (it is the only Chinese EV brand that sells in volume outside its home country), with leading roles in the EV movement in diverse geographies, from Latin America to Australia, passing by Israel and other Middle Eastern markets, and as these EV markets grow, so too will MG (and SAIC).

Although being surpassed by SAIC, the Volkswagen Group reduced its distance to the leader from 6% (19% vs 13% in Q1 2020), to the current 4% (16% vs 12%), so not all is lost for the German conglomerate, in its goal to discuss the global leadership, but what has changed in the last 12 months is that Tesla doesn't have just one competitor (VW Group) trying to catch it, but two (VWG and SAIC).

Will this mean that Tesla will lose the 2021 title? Despite an expected strong second half of the year for the VW Group, I believe Tesla will still end the year in the lead, but for 2022...All bets are on.

The BMW Group ended the first quarter of the year in the 4th place, improving on the #5 of 2020, benefiting from the implosion of the Renault-Nissan Alliance (a year ago, the Alliance had 11% share, now it has 5%...) and the popularity of its PHEV lineup.

We now have a new face on this Top 5, with Stellantis rising to 5th, with 6% share, thanks to an extensive lineup, spreaded through its 205 brands, and with the #4 BMW Group just 11.000 units ahead, we could see it run for the 4th spot soon.

Regarding the Q1 2020 ranking, we witness the disappearance of the Hyundai-Kia Group, that has seen its share drop by half, from 8% a year ago, to the current 4%, so those Hyundai Ioniq 5 and Kia EV6 are badly needed to change the fortunes of the Korean group.

BEV

Looking only at BEVs, Tesla is comfortable in the lead, with 25% share, but has lost 4% share regarding the same period of last year, but the fact that 1 in 4 BEVs sold in the World belongs to Tesla is a feat in itself, considering the current diversification process.

The Silver medal is in the hands of the 2020 Silver medalist, SAIC, with the Chinese maker jumping its share by 6%, to the current 17%, not only leaving the 3rd placed Volkswagen Group in the dust (they ended 2020 separated by just 16.000 units), but they are now starting to see Tesla's rear more clearly.

The self-registering stunt of late last year by the Volkswagen Group is now having its payback, with the first two months of the year being registration low points, with March helping it to recover a bit, but it wasn't enough to recover the 11% share that the German conglomerate had both in Q1 2020 and by the end of last year.

The self-registering stunt of late last year by the Volkswagen Group is now having its payback, with the first two months of the year being registration low points, with March helping it to recover a bit, but it wasn't enough to recover the 11% share that the German conglomerate had both in Q1 2020 and by the end of last year.

Will we see it recover significantly in Q2?

Just outside the podium we have BYD, with 5% share, with the Chinese carmaker rising one spot regarding 2020, not because it has increased its share (it was actually down from 6% to the current 5%), but because of the Renault-Nissan implosion, with the Alliance now having 4% share, a far cry from the 13%(!) it had 12 months ago...

Like in the PHEV+BEV ranking, Stellantis shows up in the Top 5 BEV ranking for the first time, in 5th, with 5% share, but despite being just 3.000 units behind the #4 BYD, do not expect it to surpass the Chinese maker anytime soon, as BYD is now set to increase deliveries significantly, now that all its BEV lineup has transitioned to the new LFP batteries.

Comparing with the BEV+PHEV table, the big defeated is the BMW Group, that due to its heavy reliance on PHEVs, it disappears from the Top 5, being replaced by the more BEV-friendly BYD.

Thursday, February 4, 2021

2020 Sales by OEM

Looking at the 2020 sales by Automotive Group, we have:

Comparing with the BEV+PHEV table, the big defeated is the BMW Group, that due to its heavy reliance on PHEVs, disappears from the Top 5, while BYD replaces it.

PHEV+BEV

If we gather plugin sales by Automotive Groups, Tesla ended the year ahead, with 16% share, 1% less than a year ago, which nevertheless is still a small feat all by itself, considering the intensive diversification process that the EV niche is now having, could have eroded more significantly its market share.

Tesla's current domination is however being threatened by the Volkswagen Group, that jumped from 6th in 2019 to the current 2nd spot, with its share jumping from 6% in 2019, to the current 13%.

More importantly, the German conglomerate reduced its distance to the leader from 227.000 units in 2019 (368k vs 141k), to the current 78.000...Inclusively, the VW Group outsold Tesla in the last quarter of the year, by registering some 191.000 units, while the Californian maker had some 183.000 deliveries.

Will this mean that VW will beat Tesla in 2021? I think it will be closer than this year, but i believe Tesla will still have the upper hand, but for 2022...All bets are on.

In 3rd place we now have Shanghai Auto, that shooted from #7 in 2019, to the Bronze medal, having seen its share jump from 6% last year to the current 9%.

But unlike Volkswagen, that had been stable at the runner-up spot since the beggining of the year, by the end of Q3 2020, the Chinese Group was still outside the Top 5, but thanks to an amazing Q4, where it had an incredible 162.000 units, it jumped to the last place of the podium, this result was much due to the thundering success of the Wuling Mini EV, that was responsible for 44% of all of SAIC's registrations. If things go on like this for the Shanghai maker in 2021, then it could become a sort of dark horse and get in the way of the much announced Tesla vs Volkswagen duel.

Regardless of what will happen in 2021, the big gainers of 2020 were the Volkswagen Group and SAIC, that counted together, gained 10% share this year.

Both the #4 Renault-Nissan Alliance and the #5 BMW Group lost 1% share regarding last year, but while the German OEM repeated the 5th spot of 2019, the Alliance lost one spot regarding the previous year, unable to resist the rise of SAIC.

Regarding the Q3 2020 ranking, we witness the disappearance of the Hyundai-Kia Group, that dropped from #4 then, to #6, despite record sales.

BEV

Looking only at BEVs, Tesla repeated the 2019 title, with 23% share, the same score it had in the previous year, a small feat considering the current diversification process.

The Silver medal changed hands a few times this year, first we had the Renault Nissan Alliance in the runner-up spot, but on Q3 the VW Group took Silver, only to lose the 2nd spot on the last quarter of the year to SAIC, that thanks to the success of its Wuling Mini EV, it came out of the Top 5 into #3 in Q3, having surpassed the German conglomerate in the last quarter.

Still, it was a positive year for the Volkswagen Group, as it jumped from 6th in 2019, with just 5% share, to the last place of the podium, with 11% share.

Still, it was a positive year for the Volkswagen Group, as it jumped from 6th in 2019, with just 5% share, to the last place of the podium, with 11% share.

Same story for SAIC, that jumped from #5 in 2019, with 6% share, to the runner-up spot, with 11% share, confirming these two Automotive Groups (SAIC and VW Group) as the winners of the year, as these two counted together earned 11% share in 2020, and the 22% of both come close to the 23% of the leader Tesla.

The Renault-Nissan Alliance was #4, with 8% share, which, funny enough, are exactly the same scores that the Alliance had in 2019.

The same can't be said regarding BYD, that was down from #3 and 9% share in 2019, to the current 5th spot and just 6%, although the Chinese Group has been recovering lately, climbing to #5 in the last quarter of the year.

Comparing with the BEV+PHEV table, the big defeated is the BMW Group, that due to its heavy reliance on PHEVs, disappears from the Top 5, while BYD replaces it.

Friday, October 30, 2020

Q1-Q3 2020 Sales by OEM

Looking at the 2020 sales by Automotive Group, we have:

PHEV+BEV

If we gather plugin sales by Automotive Groups, Tesla is ahead, with 18% share, down 1% regarding the previous June report, followed by the Volkswagen Group (13%), that increased the distance to the Renault-Nissan Alliance, to 5%, so the German conglomerate is midway between the #1 Tesla and the #3 Renault-Nissan.

And to think that 2019 ended with the Volkswagen Group in 6th, with 6% share, 2 points behind the Renault-Nissan Alliance and a whole 11 points below the leader Tesla (17%)...At this pace, the Germans could beat Tesla by Q2 2021. Bets, anyone?

Below the podium, Hyundai-Kia rose to 4th, at the expense of the BMW Group, with both keeping the 7% share they had in H1.

SAIC is now #6, with 110.000 units, benefiting from the success of the SGMW City EVs, and could displace BMW from the Top 5 by the end of the year.

With the plugin market this year growing at a 11% rate, while Tesla (+24%), Hyundai-Kia (+29%) and BMW (+17%) are growing at a slightly higher pace than average, but the Volkswagen Group is growing at warp speed (+168%), and it has been the OEM that has grown more in volume, in the past three months, beating even Tesla in that aspect.

On the other hand, the Renault-Nissan Alliance has seen its sales drop, by 1%, harmed by the slowing sales that Nissan and Mitsubishi have been experiencing. Maybe Renault could be better off seeking new dance partners (Ahem, Mercedes, Ahem)?

BEV

Looking only at BEVs, the leader Tesla (26%) lost 2% share regarding H1, but it is still 3% above the 2019 result, while the Renault Nissan Alliance continues losing share, due to Nissan's slowing sales, dropping by 1% regarding the last quarter, to 9%, and the Alliance was surpassed by the Volkswagen Group, that has kept its 10% score, which is double its final 2019 score (5%).

SAIC is also on the rise, jumping to #4, thanks to the Wuling and Baojun EVs, while increasing its share to 8%, placing the Chinese OEM 2 points ahead of last year 6% share.

Comparing with the BEV+PHEV table, the big defeated is the BMW Group, that due to its heavy reliance on PHEVs, disappears from the Top 5, to the profit of the BEV-friendly SAIC.

Comparing with the BEV+PHEV table, the big defeated is the BMW Group, that due to its heavy reliance on PHEVs, disappears from the Top 5, to the profit of the BEV-friendly SAIC.

Tuesday, February 4, 2020

2019 sales by OEM

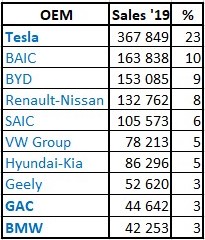

Looking at the 2019 sales by Automotive Group, we have:

PHEV+BEV

If we gather sales by Automotive Groups, Tesla is ahead, with 17% share (Up 5% regarding 2019), thanks to a 122,000 units sales growth regarding 2018, followed by BYD (10%, down 1%), that has seen its sales impacted by the subsidies change in China, and the Renault-Nissan Alliance, that dropped 1% YoY, to 9% share, that suffered from the slowing sales of the Nissan Leaf, with the 2018 podium repeating in 2019.

The #4 BAIC also dropped 1%, to 7% share (down 2%) repeating last year place, with the #5 BMW Group also keeping the same position as in 2018, but in the case of the German Group, its slight growth rate allowed it to keep the same market share as in the previous year.

The Climber in the ranking was the Volkswagen Group, that in the Year -1 of its Plan to Rule the EV World, it jumped 3 spots, from #9 to #6, surpassing SAIC, Hyundai-Kia and the Geely Group, thanks to a 59,000 units growth regarding 2018, an amazing 70% growth rate, beating even that of Tesla (+50% YoY).

Will the German Group be able to outpace Tesla again in 2020? And in 2021?

Still, despite being surpassed by Volkswagen Group, SAIC, Hyundai-Kia and Geely all grew, with the Korean Group in particular growing at a significant 38% rate.

Finally, with the demise of most of the smaller Chinese EV makers, Toyota(!) managed to climb to #10, growing 20% YoY, thanks to the start of its Chinese Operations.

BEV

Looking just at the 1.6 million BEVs, Tesla expanded its lead, doubling the result of #2 BAIC, which was also the runner-up in 2018, while the slowing sales of the Renault-Nissan Alliance dropped it to #4, with BYD becoming the 2019 Bronze medalist, thanks to a 46% growth rate, so although in the BEV+PHEV table BYD has stagnated, in reality, BYD has replaced a significant part of their plugin hybrid sales for pure electric ones.

SAIC benefits from the unexpected success of the Baojun E-Series to climb into #5, the VW Group came out of obscurity straight into #7, while Hyundai-Kia, growing 46% YoY, ended in #6.

Finally, the fast growing GAC ended at #9, and could climb even more in 2020.

Finally, the fast growing GAC ended at #9, and could climb even more in 2020.

Monday, December 30, 2019

2019 in Review - 2020 EVs

We start the 2019 review by saying goodbye to the Chevrolet Volt, nine years and 180.000 units later, the extended range plugin was an early pioneer, having been the world's Best Selling Plugin in 2012, and the runner-up in 2011 and 2013, but after the early peak of 2012 (25.370 units), sales have started to slow down, with the GM product losing contact with the first places, something that the heavily revised Volt II of 2016, despite surpassing the 2012 record, by registering 28.295 units, also failed to do, with GM's decision to not sell the 2nd generation Volt as Opel Ampera in Europe, not helping at all on the hatchback sales career.

To worsen things, the new generation was only produced for three years, with the first half of 2019 signaling the end of the EREV, with GM's supposed replacement, the Bolt EV, failing to beat the 2016 score of the Volt.

With both models, the Volt and Bolt, being quite different, it is bizarre that GM decided to kill the former when the vehicle still had a couple of years ahead and was profitable, but then again, bizarre decisions is what GM management seems to be specialist, like the refusal to sell the Gen 2 Volt in Europe, just at the time that PHEVs were all the rage in Europe...And i won't even ask why they haven't made the Volt MPV5 prototype!

Anyway, we say farewell to the pioneer Chevrolet Volt, an exciting, if cramped inside, electric vehicle, and a reference for any PHEV out there.

But back at 2019, the biggest events were:

- The coming of age of Tesla and its Model 3, after finally winning its first Manufacturers trophy in 2018, ending a three year rule of BYD, the Model 3 sweapt also that year Models trophy, 2019 cleared any doubts on wether Tesla was here to stay, with the American maker repeating both titles again, but this time with a huge 100.000 units advantage over the runner-ups. And with the Model Y, Semi, Roadster and Cybertruck on the pipeline, it looks that Tesla has at least the next two titles (2020 & '21) in the bag;

- China's subsidy changes were an earthquake in the local plugin market, originating a half-year sales rush, with the consequent fall of a cliff in Q3 and a stabilization in the doldrums in Q4. But more than a sales slump, the biggest long term consequence is the dry up of many subsidy-dependent models, while higher end nameplates, new and more competitive models from the local OEMs, like the GAC Aion S, along with quota-related introductions from foreign makers and profiting from the new environment to gain visibility, while Tesla paved the way for a strong 2020 in China, where it aims to be not only the best selling foreign maker, but also to become the first foreign OEM able to run with the best of the local brands;

- A consequence of the previous point is SAIC's lottery win with the Baojun E-Series, after a discrete career before the subsidies cut, the tiny two seater became one of the few small EVs to keep access to subsidies, propelling it to an unprecedented popularity among fleets, like car-sharing companies, becoming an unexpected bonus to the solid case that the OEM was already presenting, as it is the first Chinese EV maker to sell in (relatively) large amounts outside its domestic market, with the MG ZS EV crossover and the Maxus van, besides keeping a strong lineup of plugins across the range. If in previous years SAIC looked to be the less promising of the Chinese Big 3 (BYD, BAIC and SAIC), because it was the one to best adapt to the new environment, it is now the one to look for in China, along with the smaller GAC.

2020 EVs

Thanks to eGear.be, here is a list of what is coming and what i think of them:

Audi e-Tron Sportback - Finally some interesting looks to Audi's electric tank;

BMW iX3 - A meh! effort from BMW, a BEV version of its X3 SUV, with some middle of the road specs. The Mercedes EQC looks nicer;

FIAT 500e - With the VW EV triplets coming en force in 2020, the Italian brand had to do something , if it didn't wanted its lunch (A-segment) eaten by the German conglomerate. So in the Geneva Auto Show, they are promising a brand new 500e, with a 70.000 units target production. Unrealistic? Let's hope not, if the specs and prices are attractive, it could become a huge hit, and the automaker really needs it, because the VW triplets will pressure the other players in the city car category and FIAT without city cars in Europe...Is basically nothing.

Ford Mustang Mach-E - The reinvention of Ford? This is an OEM that seems to have seen what lied ahead (the management change surely helped), and seems to go full EV now. This new EV is really compelling and will be interesting to see the public reaction to it;

Honda e - The cutest car of 2020 and my favorite City EV, alongside the BMW i3. But that price, mmm...Will sell, but at a fraction of the i3;

Lexus UX300e - A Premium EV with an air-cooled battery, 2WD and some 300 kms range...Enough said?

Mazda MX-30 - It would be an interesting niche vehicle to add to a more mainstream EV from Mazda. But as the first mass-produced Mazda EV...Too niche.

Mercedes EQV - It won't go into the Best Sellers table, but nonetheless, it will be an interesting addition to the market, as there's nothing quite like it;

Mini Cooper Electric - After the BMW i3 being the only luxury EV on the market, the Group finally allows to launch a Mini EV, but only as a 3 door and with lower specs, and a lower price, so that it doesn't steal the i3 thunder. So yeah, it will be niche, but a good one;

Opel Corsa EV / Peugeot 208 EV - Good specs, one more techy (208), another more sporty (Corsa), both will be strong contenders to the Zoe lead in the small EV segment. Both combined could even reach 100.000 units in 2020;

Peugeot 2008 EV - Europe's Kia Niro EV. If PSA has enough batteries, it could be a huge success and reach some 50k units;

Polestar 2 - A worthy competitor to the Model 3, but most of the public won't notice it. 20k units would already be ok, 40k would be a great success;

Porsche Taycan - The only EV Elon Musk thought of being worthy to compete with Tesla. Which is saying a lot. Those 20k units allocated for 2020 could be much higher if Porsche wanted...

Tesla Model Y - Tesla Model 3, meet your nemesis. While production (200k?) of the Model Y won't be enough to displace its sibling from the Global Best Seller throne in 2020, 2021 should see it succeed to the Model 3 as the most popular EV in the World.

VW e-Up! / Seat e-Mii / Skoda Citigo EV - The triplets are the first city EVs with respectable specs and prices. Enough said. Will the triplets reach 60k units in 2020?

Volvo XC40 EV - Cousin of the Polestar 2, but with higher sales potential, because it is an SUV and Volvo is not a startup;

VW ID.3 - Along with the Tesla Model Y, the most important launch of the year. Hell, i would even say that it is the most important EV model ever, that does not wear a Tesla badge. The shape of the future of electric mobility will depend on the success of this model, that should easily surpass the 100.000 units in 2020.

Audi e-Tron Sportback - Finally some interesting looks to Audi's electric tank;

BMW iX3 - A meh! effort from BMW, a BEV version of its X3 SUV, with some middle of the road specs. The Mercedes EQC looks nicer;

FIAT 500e - With the VW EV triplets coming en force in 2020, the Italian brand had to do something , if it didn't wanted its lunch (A-segment) eaten by the German conglomerate. So in the Geneva Auto Show, they are promising a brand new 500e, with a 70.000 units target production. Unrealistic? Let's hope not, if the specs and prices are attractive, it could become a huge hit, and the automaker really needs it, because the VW triplets will pressure the other players in the city car category and FIAT without city cars in Europe...Is basically nothing.

Ford Mustang Mach-E - The reinvention of Ford? This is an OEM that seems to have seen what lied ahead (the management change surely helped), and seems to go full EV now. This new EV is really compelling and will be interesting to see the public reaction to it;

Honda e - The cutest car of 2020 and my favorite City EV, alongside the BMW i3. But that price, mmm...Will sell, but at a fraction of the i3;

Lexus UX300e - A Premium EV with an air-cooled battery, 2WD and some 300 kms range...Enough said?

Mazda MX-30 - It would be an interesting niche vehicle to add to a more mainstream EV from Mazda. But as the first mass-produced Mazda EV...Too niche.

Mercedes EQV - It won't go into the Best Sellers table, but nonetheless, it will be an interesting addition to the market, as there's nothing quite like it;

Mini Cooper Electric - After the BMW i3 being the only luxury EV on the market, the Group finally allows to launch a Mini EV, but only as a 3 door and with lower specs, and a lower price, so that it doesn't steal the i3 thunder. So yeah, it will be niche, but a good one;

Opel Corsa EV / Peugeot 208 EV - Good specs, one more techy (208), another more sporty (Corsa), both will be strong contenders to the Zoe lead in the small EV segment. Both combined could even reach 100.000 units in 2020;

Peugeot 2008 EV - Europe's Kia Niro EV. If PSA has enough batteries, it could be a huge success and reach some 50k units;

Polestar 2 - A worthy competitor to the Model 3, but most of the public won't notice it. 20k units would already be ok, 40k would be a great success;

Porsche Taycan - The only EV Elon Musk thought of being worthy to compete with Tesla. Which is saying a lot. Those 20k units allocated for 2020 could be much higher if Porsche wanted...

Tesla Model Y - Tesla Model 3, meet your nemesis. While production (200k?) of the Model Y won't be enough to displace its sibling from the Global Best Seller throne in 2020, 2021 should see it succeed to the Model 3 as the most popular EV in the World.

VW e-Up! / Seat e-Mii / Skoda Citigo EV - The triplets are the first city EVs with respectable specs and prices. Enough said. Will the triplets reach 60k units in 2020?

Volvo XC40 EV - Cousin of the Polestar 2, but with higher sales potential, because it is an SUV and Volvo is not a startup;

VW ID.3 - Along with the Tesla Model Y, the most important launch of the year. Hell, i would even say that it is the most important EV model ever, that does not wear a Tesla badge. The shape of the future of electric mobility will depend on the success of this model, that should easily surpass the 100.000 units in 2020.

Sunday, February 3, 2019

2018 Global Sales by OEM (Updated)

Looking at the 2018 sales by Automotive Group, we have:

Regarding the remaining OEMs, there is one significant change, with Hyundai-Kia surpassing the almighty VW Group and reaching #8, which says a lot about what is happening right now...

Regarding the previous post, both Tesla (12%) and BYD (11%) maintained their lead, but last year winner, the #3 Renault-Nissan Alliance (9%, -1%), lost a bit more ground, with the rising BAIC (8%, +1%) cutting distances to the podium, having surpassed BMW in November, to reach #4.

Regarding the remaining OEMs, there is one significant change, with Hyundai-Kia surpassing the almighty VW Group and reaching #8, which says a lot about what is happening right now...

Interestingly, half of the Top 10 belongs to Chinese OEMs, and if we add Tesla to the Disruptors team, Legacy OEMs are a minority in the Top 10. Is this a sign of the New World Order in the automotive industry?

Looking at last year standings, and comparing it with 2018, there are noticeable changes, Tesla jumped from #5 to the leadership, Renault-Nissan dropped from #1 to 3rd, Geely dropped two positions, to #6, SAIC was up two spots to #6, while the Volkswagen was down two spots, to #9.

Highlighting the changing times, we have two new Automotive Groups in the Top 10, with Hyundai-Kia jumping to #8, and Chery reaching #10, kicking out General Motors, now #11, and Toyota (down to #15!) out of the Top 10.

The Toyota case is particularly worrying, not only because it is one of the largest Automotive OEMs, and in this ranking is only #15, but also because in a fast growing market, it was one of the few (the only?) OEMs to lose sales (-10%) regarding 2017...

BEVs Only

Looking only at BEVs, the ranking would be like this:

1. Tesla (245.240);

2. BAIC (165.369);

3. Renault-Nissan (150.374);

4. BYD (105.420);

5. Chery (64.897).

The disruption is even more visible here, with only Renault-Nissan on the Top 5, and Tesla winning even more easily.

In fact, if we have increased this to a Top 10, we would only have another Legacy OEM here, Hyundai-Kia, #7, with 58.990 units.

So, BMW and the VW Group are still too PHEV-based to be considered one of the leading Legacy OEMs. Maybe things will look different in 2020?

BEVs Only

Looking only at BEVs, the ranking would be like this:

1. Tesla (245.240);

2. BAIC (165.369);

3. Renault-Nissan (150.374);

4. BYD (105.420);

5. Chery (64.897).

The disruption is even more visible here, with only Renault-Nissan on the Top 5, and Tesla winning even more easily.

In fact, if we have increased this to a Top 10, we would only have another Legacy OEM here, Hyundai-Kia, #7, with 58.990 units.

So, BMW and the VW Group are still too PHEV-based to be considered one of the leading Legacy OEMs. Maybe things will look different in 2020?

Subscribe to:

Comments (Atom)