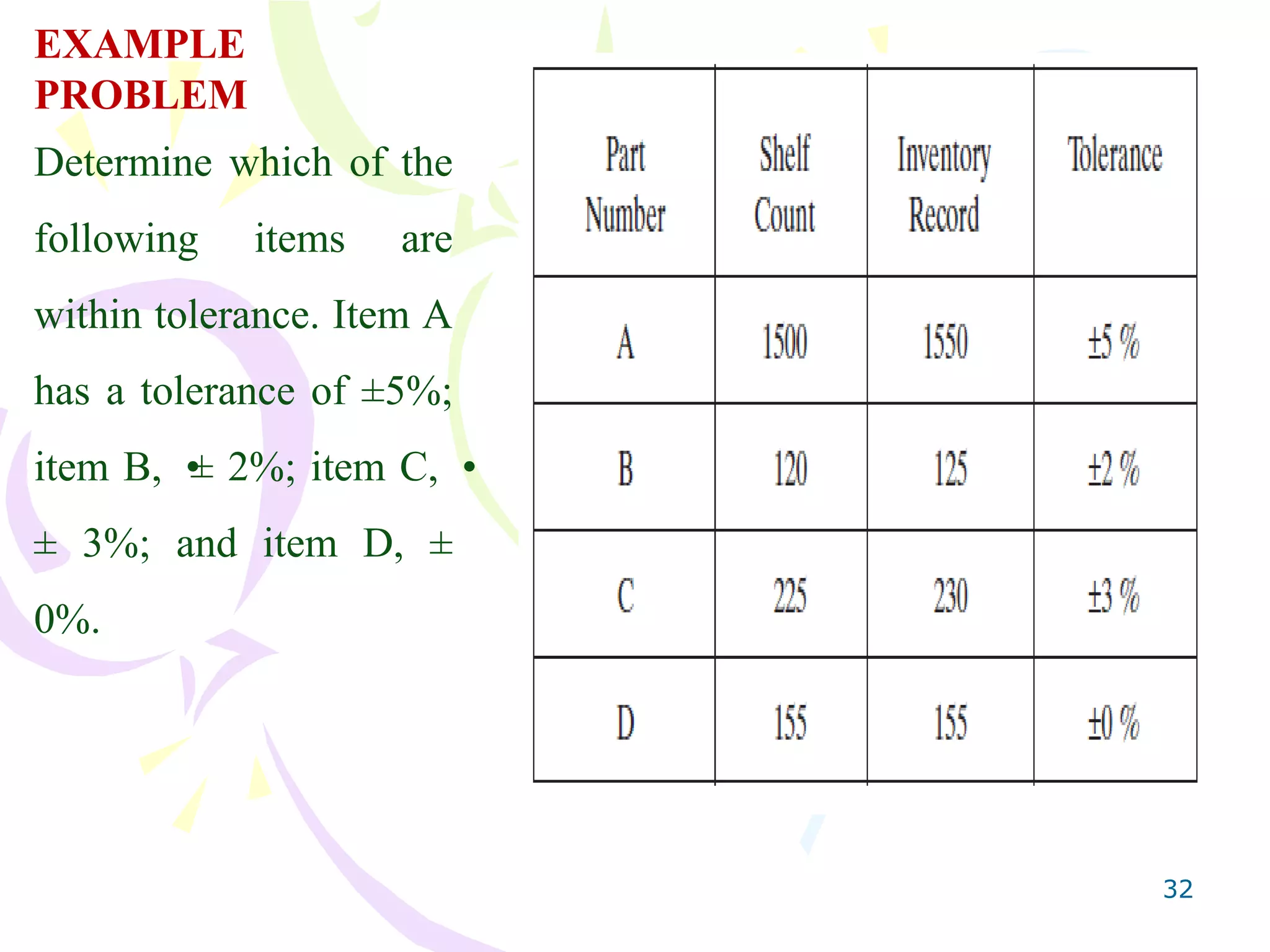

This document discusses physical inventory and warehouse management. It covers warehouse activities like receiving, storing, picking, and dispatching goods. Effective warehouse management aims to minimize costs and maximize customer service. Key aspects include warehouse layout, storage systems, inventory record accuracy, security measures, and auditing inventory through periodic physical counts and cycle counting. The accuracy of inventory records is important for supply chain planning and operations.